Bitcoin adoption is still being led by institutions. But the story in 2026 isn’t just how much they’re buying. It’s who is buying, and how they’re getting exposure.

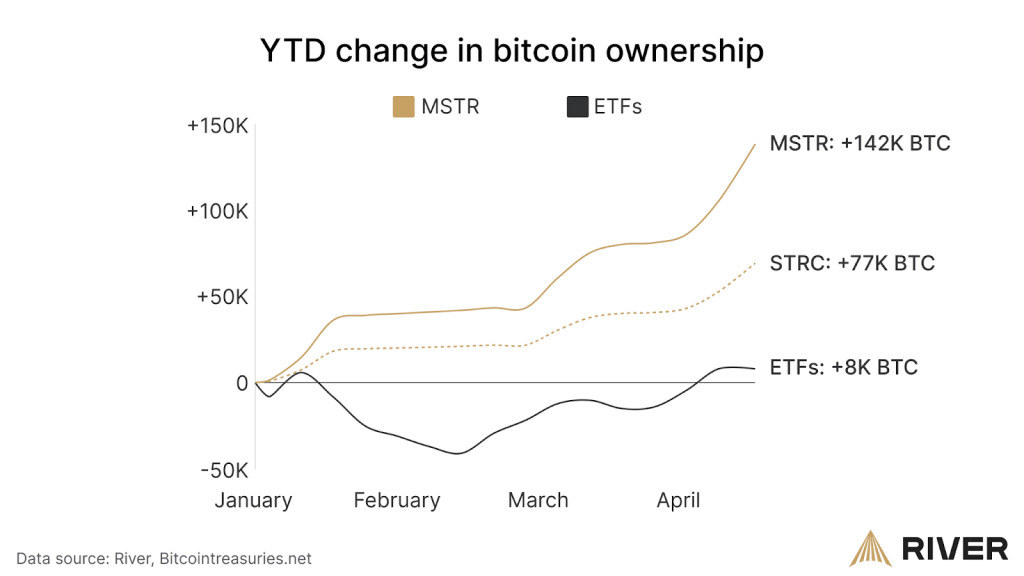

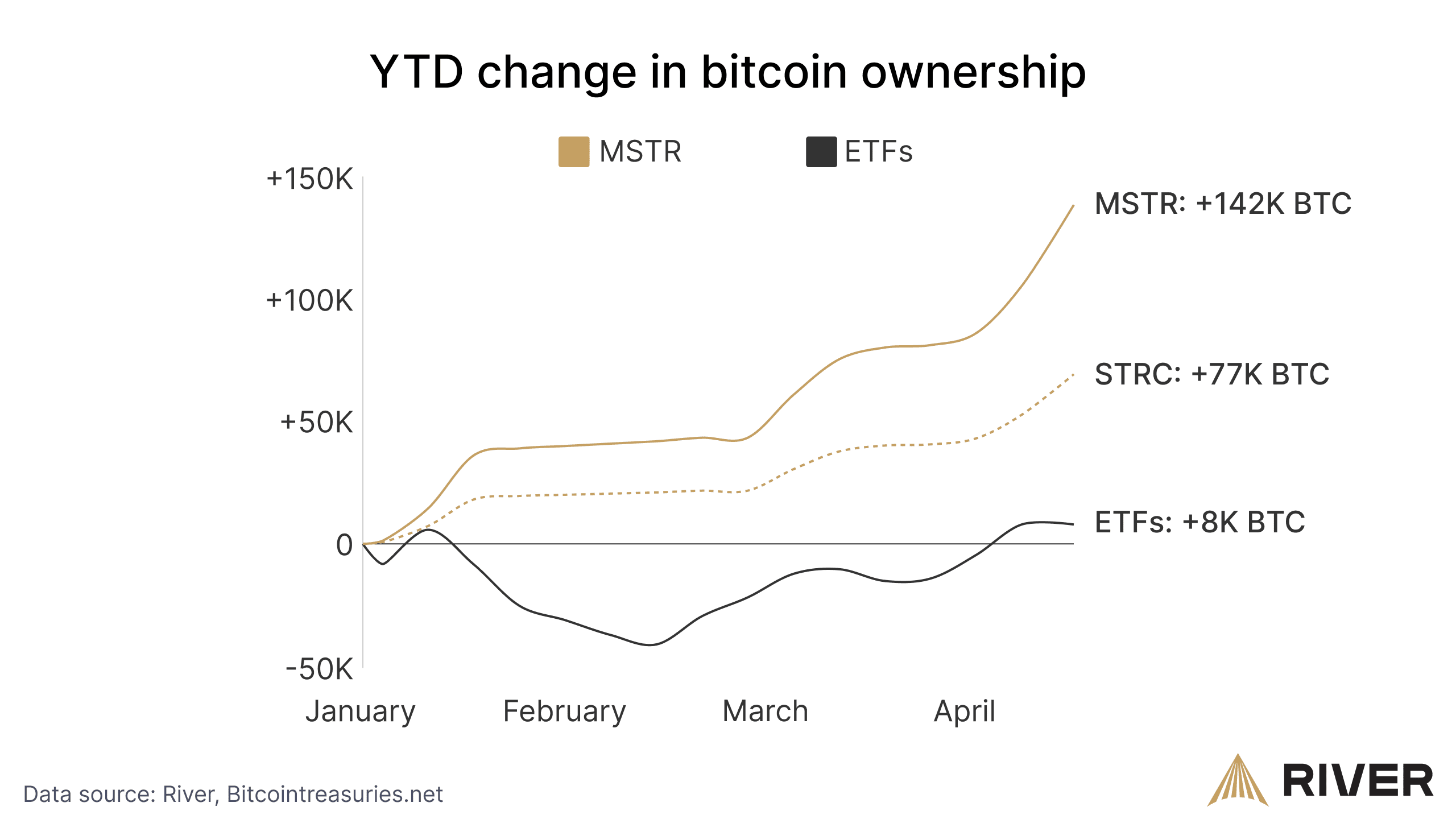

Strategy’s STRC product has bought 77,000 BTC in 2026

The largest buyer of bitcoin this year has been the bitcoin treasury company Strategy, which is now appealing to new investors through their preferred stock product STRC.

STRC accounts for roughly half of Strategy’s purchases this year. That’s 10X more bitcoin than all ETFs so far in 2026.

Designed for investors who want high income and lower price volatility than bitcoin or stocks, STRC currently pays a dividend of 11.5%. This gives investors a way to get exposure to Strategy without buying bitcoin directly. The tradeoff is that STRC investors won’t fully benefit if bitcoin rises in price significantly, but also won’t feel the full impact if it drops sharply.

STRC has become popular because it appeals to new investor types that are more risk averse than most bitcoiners. But it’s important to see STRC for what it is.

It is not bitcoin, and it is not cash. Strategy explicitly says STRC is not FDIC insured, is not collateralized by the company’s bitcoin holdings, and gives investors only a preferred claim on the residual assets of the company. That means it may appeal to income-focused investors, but it should not be confused with simply owning bitcoin itself.

Bitcoin adoption by banks is in full swing

Morgan Stanley just became the first major U.S. bank to launch its own spot bitcoin ETF, MSBT. In its first week of trading, the fund attracted more than $100 million in inflows, making it the firm’s most successful ETF launch to date.

And despite bitcoin ETFs being available for more than two years, a vast pool of institutional capital still has not entered the market. Morgan Stanley’s wealth platform includes roughly 15,000 financial advisors overseeing $2.8 trillion in client assets. Now that the firm has its own bitcoin product, even modest adoption across that network could translate into meaningful demand for bitcoin over time.

Banking, a new way to build your bitcoin position

Institutional products are not the only new engine of bitcoin demand. Another shift is happening in banking.

For decades, banks have normalized checking accounts that earn almost nothing in interest. In 2025, banks kept $434 billion in interest from Americans.

Last week, we launched banking services to challenge this model and give you a single account for your daily banking needs that earns 3.3%* on cash, paid in bitcoin. Now, instead of watching your checking balance lose ground to inflation, it’s another way to stack bitcoin.

Banking on River is just as easy as what you do today. Your cash is FDIC insured up to $250,000* and you can pay bills like credit cards, subscriptions. And there are no account fees or minimums.

*River Financial Inc. (“River”) is not a bank. USD funds are deposited by Lead Bank, Member FDIC. Your USD is FDIC-insured up to $250,000, inclusive of any deposits that you already hold at Lead Bank in the same ownership capacity. FDIC insurance may protect against a failure by Lead Bank, but does not protect against River’s failure, nor does it protect against theft or fraud. Bitcoin is not insured by the FDIC, and may lose value.

Interest may be earned on cash that has settled at Lead Bank. The current APY rate is 3.3%, and is subject to change. You may choose to receive interest payouts in Bitcoin or in USD. Lead is not affiliated with River’s Bitcoin program, products, or offerings. Not available in all states. Fees may apply. Please review the Terms of Service for eligibility restrictions and additional details.

You must be logged in to post a comment.